Please excuse my upcoming absence... I am preparing for homelessness.

The place I raved about earlier - not going to happen. Rather, the landlord won't consent to it. Our family is too large and the time is too short. So we are going to rip our family apart. The kids and I living with our family in another state, my DrH living here in medical student housing.

I am really sad. I don't like being away from my DrH that long. He doesn't like it either.

I will most likely miss his graduation. I had visions of us together, all of us, celebrating at his official graduation. Now, it will be him alone - or possible just he and I (if we can swing it).

Things don't ever turn out how you expect.

I am kicking off my long weekend early why we try to find yet another place in another state. I hope we can find something there - I don't think we can live with our family, or apart for long.

Thursday, March 29, 2012

Wednesday, March 28, 2012

Paralyzed

I am paralyzed.

Today is Monday the 26th of March. My home closes on Friday April 13th. We have 18 days to be packed up, moved out, and house cleaned up. Technically less than that unless I want to be pulling out of the driveway on the same day we are supposed to turn it over to someone else. Realistically I have 14 days.

Want to know how many boxes I have packed? NOT ENOUGH!

I have been steadily making progress, but have been on the books for a week. When you start putting books in boxes you realize that you may have an obsession. On the book shelf it didn't look like that much.

I have my boxes organized into three categories. 1) Boxes we will pack and use for the 3 months we are living somewhere else. 2) Boxes we will pack and unpack only when we arrive at our fellowship destination. 3) Boxes we will pack and will NOT unpack until we arrive at our final resting place in the future.

I love books, I can not part with them, but I know there are books that we aren't going to read in the next 1-3 years. Those books will stay in their boxes. My original intent was so that I wouldn't have to pack them up again in a year. But I am hoping that our next move includes a paid moving company with professional movers and then I won't care how much stuff I have to pack up and move out.

But for the moment, it is my headache, and I don't want to do it! I am doing a remarkable job procrastinating. This blog is providing me with ample opportunities for avoiding my elephant in the room. I should go pack something right now.

Please make this go away!

Today is Monday the 26th of March. My home closes on Friday April 13th. We have 18 days to be packed up, moved out, and house cleaned up. Technically less than that unless I want to be pulling out of the driveway on the same day we are supposed to turn it over to someone else. Realistically I have 14 days.

Want to know how many boxes I have packed? NOT ENOUGH!

I have been steadily making progress, but have been on the books for a week. When you start putting books in boxes you realize that you may have an obsession. On the book shelf it didn't look like that much.

I have my boxes organized into three categories. 1) Boxes we will pack and use for the 3 months we are living somewhere else. 2) Boxes we will pack and unpack only when we arrive at our fellowship destination. 3) Boxes we will pack and will NOT unpack until we arrive at our final resting place in the future.

I love books, I can not part with them, but I know there are books that we aren't going to read in the next 1-3 years. Those books will stay in their boxes. My original intent was so that I wouldn't have to pack them up again in a year. But I am hoping that our next move includes a paid moving company with professional movers and then I won't care how much stuff I have to pack up and move out.

But for the moment, it is my headache, and I don't want to do it! I am doing a remarkable job procrastinating. This blog is providing me with ample opportunities for avoiding my elephant in the room. I should go pack something right now.

Please make this go away!

Tuesday, March 27, 2012

Anniversary Gift to DrH

My DrH are celebrating our 8th wedding anniversary today and what did I get him? Another BOOK!

I previously mentioned that I have been packing up books. Lots and lots of books. During that process I discovered that DrH had 6 of the 7 Harry Potter books in hardcover. He was missing the very first volume. So that is what he is getting, thanks to the good folks at Amazon - I love you.

Harry Potter books, I am not sure which anniversary that is technically supposed to be but for us it will be the 8th. My DrH started reading the Harry Potter series in medical school (obviously before we met) as a way to wind down and take his mind off the heavy stuff he was studying. I teased him.

I have never read a Harry Potter Book. I think it was primarily out of rebellion. I didn't have kids when the books were in their heyday and I had other things I wanted to read. A friend of mine bought be a paperback book and 9 years later I haven't read it. I have given it to my 7 year old son.

Even though I have yet to read the books, I am sure I will to my kids (maybe), I have watched each and every one of the movies. Although I would never pay to watch them in the theater. DrH has the collection on DVD and last November we had a marathon Harry Potter movie night that technically spanned over two weeks. They were good, but I am in no way a fan in the same way he is.

I previously mentioned that I have been packing up books. Lots and lots of books. During that process I discovered that DrH had 6 of the 7 Harry Potter books in hardcover. He was missing the very first volume. So that is what he is getting, thanks to the good folks at Amazon - I love you.

Harry Potter books, I am not sure which anniversary that is technically supposed to be but for us it will be the 8th. My DrH started reading the Harry Potter series in medical school (obviously before we met) as a way to wind down and take his mind off the heavy stuff he was studying. I teased him.

I have never read a Harry Potter Book. I think it was primarily out of rebellion. I didn't have kids when the books were in their heyday and I had other things I wanted to read. A friend of mine bought be a paperback book and 9 years later I haven't read it. I have given it to my 7 year old son.

Even though I have yet to read the books, I am sure I will to my kids (maybe), I have watched each and every one of the movies. Although I would never pay to watch them in the theater. DrH has the collection on DVD and last November we had a marathon Harry Potter movie night that technically spanned over two weeks. They were good, but I am in no way a fan in the same way he is.

Monday, March 26, 2012

A Place To Rest My Head

Trying to find a place to rent for less than 3 months was proving to be difficult. With the help of our realtor we were able to find someone who was needing out of their lease at precisely the same time we need one, for exactly the amount of time we need. Another miracle from heaven in my book.

We went to look at the house/apartment and it will work. I have always wanted to live in an old house, and this fits the bill. It is 100 years old. It is an old Victorian home that has been turned in to 4 apartments. A main apartment on the lower lever, two apartments on the second, and one on the third.

The apartment that is available happens to be the main floor, thank heavens. It is really a 2 bedroom apartment but the rooms are large with closets and we aren't going to be unpacking much. It is going to be a little tight for our family of 6, but you do what you have to do!

It is near friends of ours and a popular walking/biking trail so I have a feeling we won't be spending much time actually in the unit... but maybe we will. I told my DrH that this place is exactly what I would have loved to have had for 6 years, provided it had 3 bedrooms. Who knew places like this even existed? Oh, yeah, we would have had we not been so set on buying. Now we know!

But the BEST part is the coin operated washing machine and dryer in the basement that is shared by all four units. I am going to have to load up on rolls of quarters and start baking cookies for my neighbors. We generate a lot of laundry around here!

I can't tell you how good it feels just thinking about NOT being responsible for maintaining a home. I am looking forward to renting - what a relief to not be the owner!

We went to look at the house/apartment and it will work. I have always wanted to live in an old house, and this fits the bill. It is 100 years old. It is an old Victorian home that has been turned in to 4 apartments. A main apartment on the lower lever, two apartments on the second, and one on the third.

The apartment that is available happens to be the main floor, thank heavens. It is really a 2 bedroom apartment but the rooms are large with closets and we aren't going to be unpacking much. It is going to be a little tight for our family of 6, but you do what you have to do!

It is near friends of ours and a popular walking/biking trail so I have a feeling we won't be spending much time actually in the unit... but maybe we will. I told my DrH that this place is exactly what I would have loved to have had for 6 years, provided it had 3 bedrooms. Who knew places like this even existed? Oh, yeah, we would have had we not been so set on buying. Now we know!

But the BEST part is the coin operated washing machine and dryer in the basement that is shared by all four units. I am going to have to load up on rolls of quarters and start baking cookies for my neighbors. We generate a lot of laundry around here!

I can't tell you how good it feels just thinking about NOT being responsible for maintaining a home. I am looking forward to renting - what a relief to not be the owner!

Friday, March 23, 2012

Did I Forget Anything

I know I have rambled on about budgets, income, housing, mortgages, etc. I hope I didn't scare you away, or lose you forever, but this particular topic is something I am passionate about and couldn't rest until I said everything I wanted to say.

If you have stuck out the past few weeks, thank you!

If you are interested in re-reading these posts, or directing your medical friends, I have created a new page tab that contains the links to each post in the series.

Now that I have finished my frantic writing, let me ask you:

Is there anything you would like my take on (since I so willingly give my opinion on everything)?

Feel free to contact me via email at fromadoctorswife@gmail.com or leave a comment on this post if you have suggestions for other topics.

What is next? I don't know. I do know that I need to start packing up this house, I need to move in just a few short weeks, find a place to live (2 actually), and move cross country. No problem!

Time to catch my breath and make a new plan for the next chapter in our medical history: Fellowship!

If you have stuck out the past few weeks, thank you!

If you are interested in re-reading these posts, or directing your medical friends, I have created a new page tab that contains the links to each post in the series.

Now that I have finished my frantic writing, let me ask you:

Did I miss anything? Do you have any questions for the doctors wife?

Is there anything you would like my take on (since I so willingly give my opinion on everything)?

Feel free to contact me via email at fromadoctorswife@gmail.com or leave a comment on this post if you have suggestions for other topics.

What is next? I don't know. I do know that I need to start packing up this house, I need to move in just a few short weeks, find a place to live (2 actually), and move cross country. No problem!

Time to catch my breath and make a new plan for the next chapter in our medical history: Fellowship!

Thursday, March 22, 2012

Making It Work

There is a very good chance that even after my warnings and my story, which incidentally is not as unique as you might think, you will still find yourself in a precarious financial situation.

Take a deep breath.

Do you have a plan?

Right now is the time to sit down with your spouse/significant other and talk about what your strategy will be when trouble comes. Not IF, but WHEN.

Where will that extra money come from? Not just the extra money for your regular living expenses, but the extra money for the "Oops, that wasn't supposed to happen".

Here are some examples of things that did go wrong over 6 years. But they didn't all happen in the 6th year, they came like rolling waves from the very beginning, one right after the other.

What are some options for adding extra cash to your reserves so you are prepared when IT happens?

Our story I have already shared in bits and pieces. Here is the readers digest version. Six months into our intern year (after having bought a house that would be too expensive to sell e.g., fees) we ran through our savings. In January I started working from home (with an infant and 2 year-old). I worked for a year but didn't make that much and my ability to perform my real job as wife/mother was compromised. It took up so much time and energy to juggle my responsibilities that I didn't have time to make and keep friends, or be involved in anything. I worked and took care of my family. There wasn't an extra moment.

After working for a year we found out we would be expecting again and I told my husband there was no way I could continue doing what I was doing. Our family was suffering, and with three kids everything would suffer and for what? We were both stressed nearly to the breaking point.

Making a commitment like this isn't for everyone. He had previously looked into the Military Reserves and was interested, but I didn't want him to commit. That was before we were broke, tired, stressed out. Six months later, and in the second half of PGY2 he joined the reserves.

Without their stipend there is no way we could have made it this long. The long list above... the only way we were able to take care of those things was because of the extra income we received. The only way we were able to save anything for when the next thing happened, was because of that extra income. There is no possible way we could have made it work on just his resident salary - No Way.

And it wasn't possible because we lived an extravagant lifestyle. We didn't. It wouldn't work. Our housing costs (mortgage and utilities) took up one entire paycheck plus some every single month. Don't let that happen to you!

Make your plan NOW!

Some of these we have used, others are not options, others are things I have heard of. Use it as a spring board to create your own plan.

A note about the above options: these might not be available to you.

Before you make assumptions about borrowing from family, moonlights, getting a job, etc. Make sure that is possible!

Family may not be willing or able to lend money. If you use a credit card where will the money come from to make the payments? Getting a job could prove difficult or counter-productive. Moonlighting may be prohibited. Signing with a hospital group may not be available in your specialty or they may not have a hospital in a state you are interested in working in. Getting a stipend at the beginning of residency isn't heard of very often, don't assume you will be the exception. Joining the military (we did reserves), they might not need anyone in your specialty and it doesn't happen over-night. Selling stuff, eventually you will run out of stuff to sell - then what? Cashing out long-term savings instruments can be expensive or you may not have any.

My husband had a life insurance policy his parents had set up for him, that he was paying on. Not only was it a monthly expense ($25 or something like that) it had monetary value that we needed. Maybe not the wisest decision, but he was covered through work now so we eliminated that expense and cashed out his policy. I think it amounted to $2,500 but that was money we sorely needed.

I worked prior to our getting married and had some assets in a 401(k) plan. Taking money out of retirement plans isn't something to be done lightly. It is taxed heavily, and is further penalized through the tax code. You only get about 70% of the amount you take out. It could push you into another tax bracket in some cases negating whatever gain you realized.

Take another deep breath, and make a plan. Please. You will feel better knowing it is in place even if you never need it, and I really hope you don't.

NEXT: Did I Forget Anything?

Take a deep breath.

Do you have a plan?

Right now is the time to sit down with your spouse/significant other and talk about what your strategy will be when trouble comes. Not IF, but WHEN.

Where will that extra money come from? Not just the extra money for your regular living expenses, but the extra money for the "Oops, that wasn't supposed to happen".

Here are some examples of things that did go wrong over 6 years. But they didn't all happen in the 6th year, they came like rolling waves from the very beginning, one right after the other.

- Paid off car blows head gasket, now has cracked engine block.

- Paid off car only fits 5, our family now is 6.

- Financed car loses a transmission.

- Water heater goes out.

- Air Conditioning unit goes out on July 4th:-)

- Dishwasher needs to be replaced after having been serviced twice without success.

- Deck is peeling, needs sanding and painting (twice in 6 years, probably could use it again).

- Grandparents 60th wedding anniversary and HUGE family reunion, want to go!

- Grandfather passes away, want to attend funeral.

- Sister gets married out of state, want to go!

- Baby(s) is born, not free.

- Tires need to be replaced.

- Brakes need to be replaced.

- Student loans are coming due, and can't be postponed any longer (TRUE)!

- Garage door opener gives up.

- Aluminum fascia on house blows off in wind storm needs repaired.

- Roof needs replaced.

- Trees need trimmed and they are too big for you to do.

- Grass needs fertilized, treated, weeds destroyed.

- Chimney needs cleaning.

- Lawn mower needs repaired.

- Screens torn, need repaired thanks to those big trees that didn't get trimmed in time because you have no money.

- More babies, more diapers, more beds, more food, more, more, more, more. (But I love them:-)

- Son starts school, registration fees.

- Computer crashes, needs replaced.

- Gas prices go through the roof.

- Property taxes increase.

- State income taxes increase.

- Healthcare insurance increases.

- Fellowship costs (seriously, expensive).

What are some options for adding extra cash to your reserves so you are prepared when IT happens?

Our story I have already shared in bits and pieces. Here is the readers digest version. Six months into our intern year (after having bought a house that would be too expensive to sell e.g., fees) we ran through our savings. In January I started working from home (with an infant and 2 year-old). I worked for a year but didn't make that much and my ability to perform my real job as wife/mother was compromised. It took up so much time and energy to juggle my responsibilities that I didn't have time to make and keep friends, or be involved in anything. I worked and took care of my family. There wasn't an extra moment.

After working for a year we found out we would be expecting again and I told my husband there was no way I could continue doing what I was doing. Our family was suffering, and with three kids everything would suffer and for what? We were both stressed nearly to the breaking point.

Making a commitment like this isn't for everyone. He had previously looked into the Military Reserves and was interested, but I didn't want him to commit. That was before we were broke, tired, stressed out. Six months later, and in the second half of PGY2 he joined the reserves.

Without their stipend there is no way we could have made it this long. The long list above... the only way we were able to take care of those things was because of the extra income we received. The only way we were able to save anything for when the next thing happened, was because of that extra income. There is no possible way we could have made it work on just his resident salary - No Way.

And it wasn't possible because we lived an extravagant lifestyle. We didn't. It wouldn't work. Our housing costs (mortgage and utilities) took up one entire paycheck plus some every single month. Don't let that happen to you!

Make your plan NOW!

Some of these we have used, others are not options, others are things I have heard of. Use it as a spring board to create your own plan.

- Borrow from family

- Use credit card

- Obtain work

- Moonlight

- Signing with a large hospital affiliation, like HCA

- Getting a stipend from a specific group or hospital that you will commit to

- Joining the military full-time or reserves

- Selling valuables

- Cash out stock, life insurance policies, 401(k)

A note about the above options: these might not be available to you.

Before you make assumptions about borrowing from family, moonlights, getting a job, etc. Make sure that is possible!

Family may not be willing or able to lend money. If you use a credit card where will the money come from to make the payments? Getting a job could prove difficult or counter-productive. Moonlighting may be prohibited. Signing with a hospital group may not be available in your specialty or they may not have a hospital in a state you are interested in working in. Getting a stipend at the beginning of residency isn't heard of very often, don't assume you will be the exception. Joining the military (we did reserves), they might not need anyone in your specialty and it doesn't happen over-night. Selling stuff, eventually you will run out of stuff to sell - then what? Cashing out long-term savings instruments can be expensive or you may not have any.

My husband had a life insurance policy his parents had set up for him, that he was paying on. Not only was it a monthly expense ($25 or something like that) it had monetary value that we needed. Maybe not the wisest decision, but he was covered through work now so we eliminated that expense and cashed out his policy. I think it amounted to $2,500 but that was money we sorely needed.

I worked prior to our getting married and had some assets in a 401(k) plan. Taking money out of retirement plans isn't something to be done lightly. It is taxed heavily, and is further penalized through the tax code. You only get about 70% of the amount you take out. It could push you into another tax bracket in some cases negating whatever gain you realized.

Take another deep breath, and make a plan. Please. You will feel better knowing it is in place even if you never need it, and I really hope you don't.

NEXT: Did I Forget Anything?

Wednesday, March 21, 2012

Renting Myths Debunked

I know many people feel that renting a home is like throwing money away. I hope in my previous posts I have adequately demonstrated that sometimes owning a home IS throwing money away!

Public policy is partly to blame for the negative stigma attached to renting. I found this article in my research that you might find interesting. You might be thinking that you could use the tax advantage associated with paying interest. Calculate that very carefully. If you don't have enough deductions to itemize you will take the standard deduction anyway. Taxes = politics and politics can change. The mortgage interest deduction may not always be around.

Let me remind you that we are a unique group, but we are still in training. There will be time for home ownership later. This is the time to enjoy the consistency and security that comes with renting a home or apartment. Let someone else be responsible for the maintenance, replacement, upkeep, potential depreciation, wear and tear, etc that comes with home ownership.

Owning a home is not all it is cracked up to be! When you rent, you know what your rent is. When you own you never know what problem is waiting around the corner or when it will strike. I might add that it will never come at a good time, and you will never have the money when it does. When you rent, you have someone to call to fix what is broken. If they don't fix it you have recourse. When you own your home, there is no one to call unless you have the money:-)

I could never have dreamed of the expenses we incurred just in maintenance. Owning a home has an untold number of hidden expenses that I have tried to detailed. The fees getting in, the maintenance staying in, and the fees getting out. All of which are expenses that are associated only with owning.

You may make the mistake of thinking that you don't need to worry about what happens when you go to sell because you will be a rich doctors' wife. Don't take that naive approach to this very important decision.

There are too many variables that can sabotage your best intentions. You don't have to look very hard to find someone whose:

Public policy is partly to blame for the negative stigma attached to renting. I found this article in my research that you might find interesting. You might be thinking that you could use the tax advantage associated with paying interest. Calculate that very carefully. If you don't have enough deductions to itemize you will take the standard deduction anyway. Taxes = politics and politics can change. The mortgage interest deduction may not always be around.

Let me remind you that we are a unique group, but we are still in training. There will be time for home ownership later. This is the time to enjoy the consistency and security that comes with renting a home or apartment. Let someone else be responsible for the maintenance, replacement, upkeep, potential depreciation, wear and tear, etc that comes with home ownership.

Owning a home is not all it is cracked up to be! When you rent, you know what your rent is. When you own you never know what problem is waiting around the corner or when it will strike. I might add that it will never come at a good time, and you will never have the money when it does. When you rent, you have someone to call to fix what is broken. If they don't fix it you have recourse. When you own your home, there is no one to call unless you have the money:-)

I could never have dreamed of the expenses we incurred just in maintenance. Owning a home has an untold number of hidden expenses that I have tried to detailed. The fees getting in, the maintenance staying in, and the fees getting out. All of which are expenses that are associated only with owning.

You may make the mistake of thinking that you don't need to worry about what happens when you go to sell because you will be a rich doctors' wife. Don't take that naive approach to this very important decision.

There are too many variables that can sabotage your best intentions. You don't have to look very hard to find someone whose:

- Residency programs closes

- Program isn't a good fit

- Husband changed their minds about specialties

- Husband decided to do a fellowship:-)

When you own a home you are tied down. It is a burden you will carry every month, every year.

I hope the housing market recovers enough to provide families a sense of security in owning a home. I really do. Buying a home was never intended to be a short-term situation. For people who will be living in their home a long time, buying and paying that mortgage off as quickly as possible is a great idea. For those of us just passing through the last thing we need is a mortgage and house to take care of.

Remember you are not like everyone else. This financial situation is temporary for you. Your light at the end of the tunnel is at least a light! Because your future is different, making money (or losing it) on a house is not something you need to be concerned with.

Right now your job is to get trained and move on. What is an immediate concern is providing for yourself and your family. The best way to do that is to eliminate unnecessary risk. Owning a home right now is an unnecessary risk. Your budget will have a better chance of survival if you can keep your largest monthly expense constant, no surprises, no hidden fees.

I love this quote by Dave Ramsey,

IF YOU WILL LIVE LIKE NO ONE ELSE,

LATER YOU CAN LIVE LIKE NO ONE ELSE!

Your time will come! It will be here before you know it!

I know you have dreams of decorating and painting. Guess what? Many landlords will let you do whatever you want, provided it is tasteful or is painted the original color when you leave. Don't let yourself get hung up on paint! The good news is that there are many people in tough situations who need to rent their homes - there is no shortage of rentals.

Entire industries exist telling you that buying a home is always the right decision. Realtors (I know I have at least one realtor reader:-) make commissions every time a home is sold. In the last 6 years our home has generated $17,000 in brokerage fees alone.

HGTV would have us believe that we can take any house and with a couple hundred dollars turn it into a magazine worthy show piece. Home Improvement stores are like Disneyland to a person who owns a home! Home inspectors, appraisers, radon mitigators all profit from the buying/selling of homes. Local governments must love the constant turn-over, they collect transfer taxes. Bankers will let you borrow more than you should. Home buying and selling might not be a good deal for you, but it is a heck of a deal for everyone else.

HGTV would have us believe that we can take any house and with a couple hundred dollars turn it into a magazine worthy show piece. Home Improvement stores are like Disneyland to a person who owns a home! Home inspectors, appraisers, radon mitigators all profit from the buying/selling of homes. Local governments must love the constant turn-over, they collect transfer taxes. Bankers will let you borrow more than you should. Home buying and selling might not be a good deal for you, but it is a heck of a deal for everyone else.

The only person looking out for your best interests is YOU! The only person who is concerned about the welfare of your family is YOU! The only person who can make this very important decision is YOU!

Next: Making It Work

Tuesday, March 20, 2012

When It Is Time To Sell

This is the final (I think) story in my housing saga.

We sold our house!!! Yeah and congratulations to us. It was on the market for 5 days, sold for $500 less than our asking price. We close on April 13, 2012. Why am I not happy?

When you buy a house the last thing on your mind is selling it, but I suggest you may want to consider it first. We have sold our house too early! Which I agree is better than selling too late. Homes in our area are on the market an average of 57 days. That would have been perfect, and what we were counting on. We don't finish residency until June 30 and will be homeless on April 13.

Why homeless? Because finding a rental property for 3 months is nearly impossible unless you are willing to pay for 6 months. So.... our options at the moment are:

Next: Renting Myths Debunked.

We sold our house!!! Yeah and congratulations to us. It was on the market for 5 days, sold for $500 less than our asking price. We close on April 13, 2012. Why am I not happy?

When you buy a house the last thing on your mind is selling it, but I suggest you may want to consider it first. We have sold our house too early! Which I agree is better than selling too late. Homes in our area are on the market an average of 57 days. That would have been perfect, and what we were counting on. We don't finish residency until June 30 and will be homeless on April 13.

Why homeless? Because finding a rental property for 3 months is nearly impossible unless you are willing to pay for 6 months. So.... our options at the moment are:

- DrH live with a friend (or sleep in the call room), kids and I drive across country and stay with our family.

- Temporary corporate suites (hotel) at $3,000/month

- Kids and I go to fellowship location early and wait.

- Live in a friends house that is for sale, unless she sells it before then.

- Find someone who is wanting out of their lease and just the right time.

I don't know where we are living!

Hint: if we had been renting we would just tell our landlord when we will be vacating the premises. Much easier! Something to think about.

But the purpose of this post is to wrap up the costs associated with owning a home. Buying a home costs a little up front. Owning the home, costs a fair amount, if you keep it up. Selling a home is an expensive endeavor.

To recap expenses up to this point:

Settlement/Closing fees at time of purchase: $3,331.09

Improvements/Maintenance to home: $20,000

Settlement/Closing fees SOLD $ 11,828

Total Expenses = $35,159 (not including depreciation)

This is how those seller closing fees breakdown (this is from our estimated proceeds sheet, which I told my realtor the name should be changed because there are NO proceeds).

State Taxes ($1.50/$1,000) = $201.60

Title Policy ($4.00/$1,000) = $537.60

Release of Mortgage = $40

Home Warranty to Buyer = $475

Attorney Fee= $300

Brokerage Fee (6%) = $8,064.00

Property Taxes = $1,075 (partial year)

Radon Mitigation = $800

Inspection repairs = $335

Total = $11,828

Here is another way to look at how much owning a house has cost us over the last 6 years.

Getting in the house = $3,331.09

Staying in the house = $20,000

Getting out of the house = $11,828

Total = $35,159

This total represents real dollars associated with buying, selling, and maintaining a home. This is money directly from our pocket. This is money that had nothing to do with paying our mortgage payment every month.

Let me put it in perspective this way. Even if we didn't make a single repair or improvement, just the total fees of getting in and out of a house for our family totaled $15,159.09. We will have been in this house for 69 months. Those fees divided by 69 months equals a cost of $220. That is what it cost us each month to live in this house in just fees! And the fees would be the same regardless of how long we stayed here. One year or ten, the fees are based off the purchase price and have nothing to do with how long you have owned the home. The shorter the stay the more expensive the fees per month. The longer the stay the less expensive.

For all of that expense what did we get in return?

After we payoff our mortgage balance of $128,000 and pay our closing fees of $11,828 we will still have to pay $5,428 to sell our house. That is money directly out of our "deep" pockets.

Between equity lost, fees, and improvements the total amount we have lost is $45,759.

I can hear you! You just said that things are different now. Really? Tell me about it in 5 years, maybe it will be. Maybe it won't. Are you willing to take that risk?

Settlement/Closing fees SOLD $ 11,828

Total Expenses = $35,159 (not including depreciation)

This is how those seller closing fees breakdown (this is from our estimated proceeds sheet, which I told my realtor the name should be changed because there are NO proceeds).

State Taxes ($1.50/$1,000) = $201.60

Title Policy ($4.00/$1,000) = $537.60

Release of Mortgage = $40

Home Warranty to Buyer = $475

Attorney Fee= $300

Brokerage Fee (6%) = $8,064.00

Property Taxes = $1,075 (partial year)

Radon Mitigation = $800

Inspection repairs = $335

Total = $11,828

Here is another way to look at how much owning a house has cost us over the last 6 years.

Getting in the house = $3,331.09

Staying in the house = $20,000

Getting out of the house = $11,828

Total = $35,159

This total represents real dollars associated with buying, selling, and maintaining a home. This is money directly from our pocket. This is money that had nothing to do with paying our mortgage payment every month.

Let me put it in perspective this way. Even if we didn't make a single repair or improvement, just the total fees of getting in and out of a house for our family totaled $15,159.09. We will have been in this house for 69 months. Those fees divided by 69 months equals a cost of $220. That is what it cost us each month to live in this house in just fees! And the fees would be the same regardless of how long we stayed here. One year or ten, the fees are based off the purchase price and have nothing to do with how long you have owned the home. The shorter the stay the more expensive the fees per month. The longer the stay the less expensive.

For all of that expense what did we get in return?

Purchase price in 2006: $145,000

Selling Price in 2012: $134,400

Value Lost = $10,600 - this represents that portion of our mortgage payment that was applied to principle every month, gone.

Between equity lost, fees, and improvements the total amount we have lost is $45,759.

I can hear you! You just said that things are different now. Really? Tell me about it in 5 years, maybe it will be. Maybe it won't. Are you willing to take that risk?

Next: Renting Myths Debunked.

Monday, March 19, 2012

Rent To Own

We are all familiar with the concept of rent to own. Hopefully, not from personal experience.

It works like this: You don't have any money for a washing machine, furniture, computer. You don't have adequate credit to borrow. You want something now but have no money. In many of these cases the buyers who rent to own end up paying nearly twice as much for an item than they would have if they had the money to buy it.

We are so much smarter than that, we would never think about renting to own anything. We can smell a trap when we see it.

BUT, we fall for it when it comes to our homes. We can't afford them. We don't have any money. Everybody has one. We want one. So we borrow the money and essentially "rent to own" a house.

When you sign your mortgage documents you will receive a large stack of papers. One of which will be a disclosure statement with the following information:

Your Annual Percentage Rate - the cost of your credit as a yearly rate.

Finance Charge - the dollar amount the credit will cost you.

Amount Financed - the amount of credit provided to you.

Total of Payments* - The amount I will have paid after I have made all payments as scheduled.

*note this amount is only the principle and interest, it doesn't include the property tax or insurance you will also pay.

What if I told you, that if you were to finance your home with a 30 year mortgage and made payments for those 30 years (without refinancing, or taking out a 2nd mortgage against your equity, etc) that you will come close to paying double. Sounds like rent to own to me.

It is true.

This is what our Disclosure Statement(s) told us

APR 4.925% (2009 - I know they are lower now)

Finance Charge $114,475

Amount Financed $137,206

Total Payments $251,691

You will also receive an amortization schedule that will map out when each payment is due, and if paid on that date, what amount will be paid towards interest and towards principle. It is a fascinating document. You can play with one here.

But that is just part of the story. You will inevitably spend money on your house which will increase your actual costs of owning a home outside of the mortgage.

I have already warned my husband that we will never have a 30 year mortgage. I don't care how long we have to wait.

Next: When It Is Time To Sell - The Final Story.

It works like this: You don't have any money for a washing machine, furniture, computer. You don't have adequate credit to borrow. You want something now but have no money. In many of these cases the buyers who rent to own end up paying nearly twice as much for an item than they would have if they had the money to buy it.

We are so much smarter than that, we would never think about renting to own anything. We can smell a trap when we see it.

BUT, we fall for it when it comes to our homes. We can't afford them. We don't have any money. Everybody has one. We want one. So we borrow the money and essentially "rent to own" a house.

When you sign your mortgage documents you will receive a large stack of papers. One of which will be a disclosure statement with the following information:

Your Annual Percentage Rate - the cost of your credit as a yearly rate.

Finance Charge - the dollar amount the credit will cost you.

Amount Financed - the amount of credit provided to you.

Total of Payments* - The amount I will have paid after I have made all payments as scheduled.

*note this amount is only the principle and interest, it doesn't include the property tax or insurance you will also pay.

What if I told you, that if you were to finance your home with a 30 year mortgage and made payments for those 30 years (without refinancing, or taking out a 2nd mortgage against your equity, etc) that you will come close to paying double. Sounds like rent to own to me.

It is true.

This is what our Disclosure Statement(s) told us

APR 4.925% (2009 - I know they are lower now)

Finance Charge $114,475

Amount Financed $137,206

Total Payments $251,691

You will also receive an amortization schedule that will map out when each payment is due, and if paid on that date, what amount will be paid towards interest and towards principle. It is a fascinating document. You can play with one here.

But that is just part of the story. You will inevitably spend money on your house which will increase your actual costs of owning a home outside of the mortgage.

I have already warned my husband that we will never have a 30 year mortgage. I don't care how long we have to wait.

Next: When It Is Time To Sell - The Final Story.

Friday, March 16, 2012

The Mortgage Payment Breakdown

If you are considering buying a home I recommend reading/watching a series of articles/videos that I discovered while writing this post (here).

There are so many factors that go into determining your particular mortgage payment. The same price house, with the same interest rate will not be the same in every state.

When we first started looking for houses it was easy to get excited about all the affordable houses we found. And we were excited! I know you are, too. We would search Realtor.com and other housing websites to see what was available in our "supposed" price range and become giddy at how seemingly cheap houses were compared to where we lived. You have seen them too. You find a house you like and over in the corner they give you a number of what the approximate mortgage will be.

That LOW number only to tells a small portion of the story. The low number is the one that hooks you and gets you thinking you can do this. Your mortgage payment will not be that low.

Many of those sites do not have accurate information, or any, regarding the current property taxes assessed on that particular home. Depending on your state, property taxes could represent a significant portion of your mortgage.

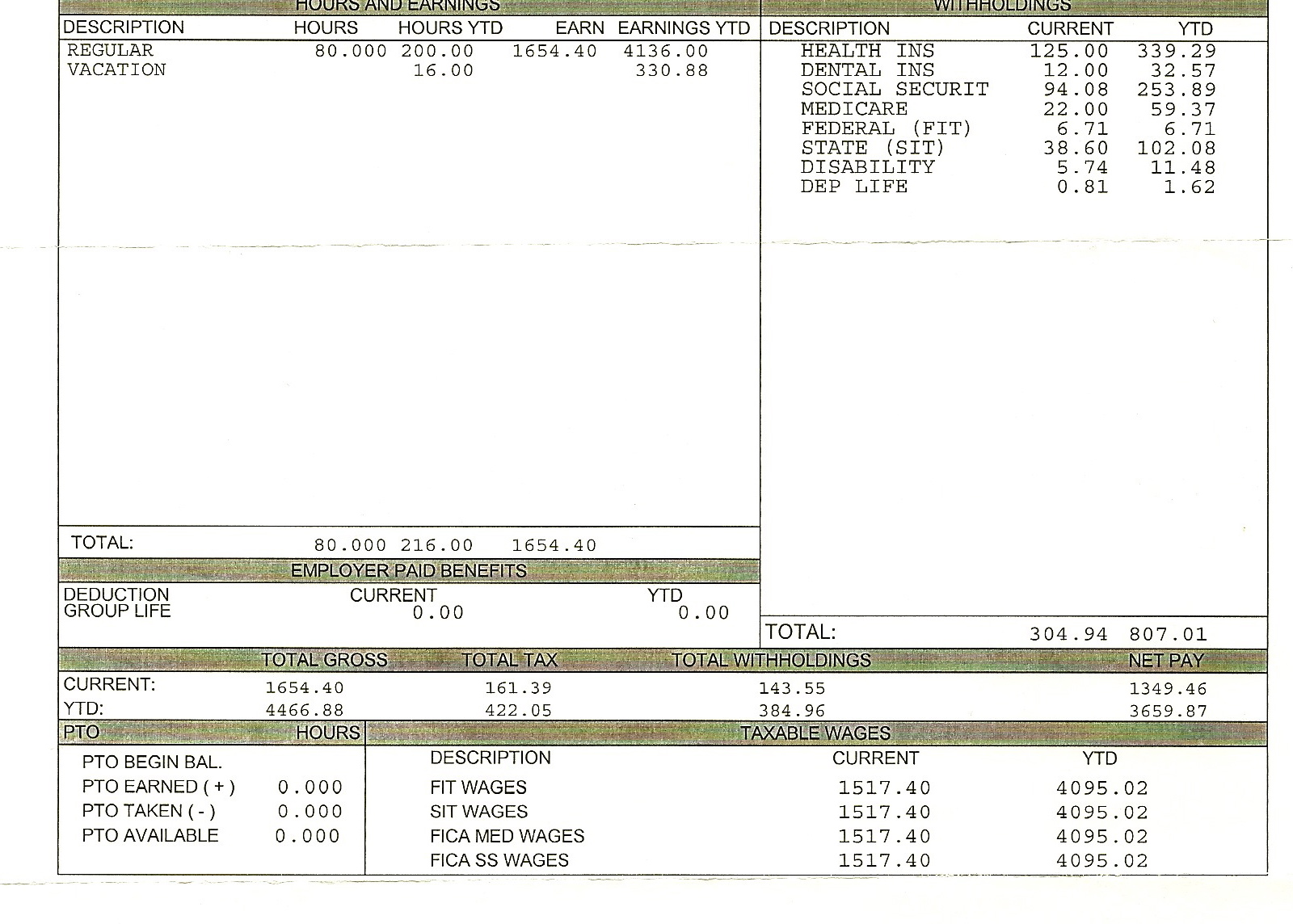

Since I have been using myself as an example, here is what our current mortgage payments look like 5.5 years into our mortgage.

Monthly payment: $1,167

Principle: $308.64

Interest: $539.80

Property Taxes: $260

Insurance (property/flood): $60

When I look at the total amounts we have paid over the years (5.5) this is how they breakdown into percentages

57.37% Interest - this is money that you pay the bank for the pleasure of using their money instead of your own to gamble with.

20.26% Property Taxes - this is the amount you pay to your city/county that funds schools, local projects, etc. - unlike a fixed rate mortgage, your property tax may increase every year like ours did.

17.32% Principle - this is your real contribution that becomes equity assuming your house is still worth what you bought it for.

5.05% Homeowners Insurance/Flood Insurance - this is what the bank requires you to have to protect their investment should something happen to the property.

Having a mortgage of any size is in reality using someone else's money to invest with the hopes that the investment pays off. You assume all of the risk and you pay a hefty price for that arrangement.

Next: Rent To Own = Mortgage

There are so many factors that go into determining your particular mortgage payment. The same price house, with the same interest rate will not be the same in every state.

When we first started looking for houses it was easy to get excited about all the affordable houses we found. And we were excited! I know you are, too. We would search Realtor.com and other housing websites to see what was available in our "supposed" price range and become giddy at how seemingly cheap houses were compared to where we lived. You have seen them too. You find a house you like and over in the corner they give you a number of what the approximate mortgage will be.

That LOW number only to tells a small portion of the story. The low number is the one that hooks you and gets you thinking you can do this. Your mortgage payment will not be that low.

Many of those sites do not have accurate information, or any, regarding the current property taxes assessed on that particular home. Depending on your state, property taxes could represent a significant portion of your mortgage.

Since I have been using myself as an example, here is what our current mortgage payments look like 5.5 years into our mortgage.

Monthly payment: $1,167

Principle: $308.64

Interest: $539.80

Property Taxes: $260

Insurance (property/flood): $60

When I look at the total amounts we have paid over the years (5.5) this is how they breakdown into percentages

57.37% Interest - this is money that you pay the bank for the pleasure of using their money instead of your own to gamble with.

20.26% Property Taxes - this is the amount you pay to your city/county that funds schools, local projects, etc. - unlike a fixed rate mortgage, your property tax may increase every year like ours did.

17.32% Principle - this is your real contribution that becomes equity assuming your house is still worth what you bought it for.

5.05% Homeowners Insurance/Flood Insurance - this is what the bank requires you to have to protect their investment should something happen to the property.

Having a mortgage of any size is in reality using someone else's money to invest with the hopes that the investment pays off. You assume all of the risk and you pay a hefty price for that arrangement.

Next: Rent To Own = Mortgage

Thursday, March 15, 2012

How Much Does Buying A House Cost

If you don't have any money to put down on a house that should be your first indication that you have no business buying a house. Even if you have a little down payment, you should consider renting and keeping that down payment as an emergency fund!

It is harsh, but it is true. If you haven't been able to save anything of consequence before buying a house, your chances of accumulating any savings when you do buy a house are next to zero. If you aren't able to save anything you will not be able to maintain your house, or your car, or your kids.

I remember being a young twenty something and wanting to buy a car. At the time I didn't have a car payment, but had a car - I just wanted a nicer one. My dad suggested that I "test drive" my car payment before I committed to it. He said to pretend to make car payments to my savings account for 6 months. If I was able to do that I probably would be able to make the payments and would have a down-payment to add to it. My parents didn't drive a nice car, shy would I listen to them? Parents are so wise, and we think they are so foolish. What makes them so wise? They have been down this road before. I am not saying I am wise, but I've been down the road. By the way, I didn't even try his way - I should have.

Not that long ago people used to have 20% of the purchase price as a down payment. Why? It demonstrated financial responsibility! Slowly over the years it became less and less and now we are in the place we are today where people can buy a house with almost "zero" of their own money.

People who demonstrated no financial accountability (measured by savings) were able to buy houses. They gave us one (and we even put some down), what were they thinking! One little bump in the road and life gets hard real fast. It gets hard for you, it doesn't get hard for the bank. No one at the bank is losing any sleep over the fact that you are (or will be) struggling.

Here is a basic truth about money that can explain why things get more expensive (e.g., tuition, houses, etc). When money becomes cheap and easy to acquire then the actual price of things matters very little. The only thing that matters is can I afford the monthly payment. Who cares how long those payments will be required.

What difference does the price of my tuition make when I am not actually going to pay for it. I will eventually, but not now. What difference does the price of my home make when I am not going to pay for it right now. I will eventually, but not now. Or in most cases because no one stays in their home very long they are just "renting" from the bank with no intention of actually owning that home.

I went over my loan documents from our home purchase in 2006, here are the facts about the costs associated with just getting into a home. (Yes, I know this is just one example and there are others - some more, some less - it is an example, a real-world example).

The agreed upon sales price for our home in 2006: $145,000

Settlement charges/closing costs: $3,372.42

Gross amount due from borrower (that's me/you): $148,372.42

Mortgage amount: $137,636

Down payment: $7,225.89

Credit from seller: $1,000 (to fix sinking driveway, that amount only covered 25%)

Property Tax credit for previous year: $2,510.53

Total: $148,372.42

May I direct your attention to two items: settlement/closing costs & down payment

What were the settlement charges paid by the borrower (me/you)?

When we purchased our house in 2006 the interest rate we received at the time was 6.674%. Guess what, interest rates dropped and we refinanced our home in 2009, exactly 3 years later. We were fairly confident that all would be well. Our home had increased in value by $8,000 and we were making improvements that would increase its value (or so we thought). But the real reason we refinanced was that our budget was squeezed and we needed more money in our pockets every month. We had just had another baby, making us a family of 5.

We refinanced from 6.674% (2006) to 4.925% (2009). A difference of almost 2 percentage points made a significant different in our payments. From $953 to $827 (PI), a savings of $126 per month over the next three years.

BUT refinancing comes with it's own costs too: $3,154.03

Before you start saying that it looks like we made some poor financial decisions, let me remind you that when you are getting squeezed by your budget you will start to make choices that under other circumstances you would not. And you will justify it by saying it is the responsible thing to do. No one wants to pay more in interest than they have to! But in the long run whatever we saved was essentially wasted on fees, and additional interest. In the short term we survived another day.

When I total all the fees that were associated with this house in both obtaining a mortgage and then refinancing it (not counting property taxes) we spent $1,842.99 the first time and $1,488.10 the second time for a grand total of $3,331.09.

$3,331.09 for FEES and we are going to have thousands more in fees when it closes (that post will be fun). Regardless of what the housing market, or interest rates are doing there are fees everywhere! Fewer on the front end, and more on the back end. There is no way around it when you buy.

Owning a house is EXPENSIVE getting in, staying in, and getting out.

Next: The Mortgage Payment Breakdown

It is harsh, but it is true. If you haven't been able to save anything of consequence before buying a house, your chances of accumulating any savings when you do buy a house are next to zero. If you aren't able to save anything you will not be able to maintain your house, or your car, or your kids.

I remember being a young twenty something and wanting to buy a car. At the time I didn't have a car payment, but had a car - I just wanted a nicer one. My dad suggested that I "test drive" my car payment before I committed to it. He said to pretend to make car payments to my savings account for 6 months. If I was able to do that I probably would be able to make the payments and would have a down-payment to add to it. My parents didn't drive a nice car, shy would I listen to them? Parents are so wise, and we think they are so foolish. What makes them so wise? They have been down this road before. I am not saying I am wise, but I've been down the road. By the way, I didn't even try his way - I should have.

Not that long ago people used to have 20% of the purchase price as a down payment. Why? It demonstrated financial responsibility! Slowly over the years it became less and less and now we are in the place we are today where people can buy a house with almost "zero" of their own money.

People who demonstrated no financial accountability (measured by savings) were able to buy houses. They gave us one (and we even put some down), what were they thinking! One little bump in the road and life gets hard real fast. It gets hard for you, it doesn't get hard for the bank. No one at the bank is losing any sleep over the fact that you are (or will be) struggling.

Here is a basic truth about money that can explain why things get more expensive (e.g., tuition, houses, etc). When money becomes cheap and easy to acquire then the actual price of things matters very little. The only thing that matters is can I afford the monthly payment. Who cares how long those payments will be required.

What difference does the price of my tuition make when I am not actually going to pay for it. I will eventually, but not now. What difference does the price of my home make when I am not going to pay for it right now. I will eventually, but not now. Or in most cases because no one stays in their home very long they are just "renting" from the bank with no intention of actually owning that home.

I went over my loan documents from our home purchase in 2006, here are the facts about the costs associated with just getting into a home. (Yes, I know this is just one example and there are others - some more, some less - it is an example, a real-world example).

The agreed upon sales price for our home in 2006: $145,000

Settlement charges/closing costs: $3,372.42

Gross amount due from borrower (that's me/you): $148,372.42

Mortgage amount: $137,636

Down payment: $7,225.89

Credit from seller: $1,000 (to fix sinking driveway, that amount only covered 25%)

Property Tax credit for previous year: $2,510.53

Total: $148,372.42

May I direct your attention to two items: settlement/closing costs & down payment

What were the settlement charges paid by the borrower (me/you)?

- appraisal fee $275

- credit report $20

- commitment fee $255

- underwriting fee $150

- flood zone certification $11

- interest 6/16/2006-7/1/2006 $315.82

- hazard insurance $186.51

- county property taxes $1529.43

- aggregate account adjustment -$124.34

- settlement or closing fee $100

- attorney's fee $300

- title insurance $133

- recording fees $51

- mortgage recording fee $23

- state surcharge fees $40

- assignment recording fee $21

- overnight fee $15

- POA recording fee $21

When we purchased our house in 2006 the interest rate we received at the time was 6.674%. Guess what, interest rates dropped and we refinanced our home in 2009, exactly 3 years later. We were fairly confident that all would be well. Our home had increased in value by $8,000 and we were making improvements that would increase its value (or so we thought). But the real reason we refinanced was that our budget was squeezed and we needed more money in our pockets every month. We had just had another baby, making us a family of 5.

We refinanced from 6.674% (2006) to 4.925% (2009). A difference of almost 2 percentage points made a significant different in our payments. From $953 to $827 (PI), a savings of $126 per month over the next three years.

BUT refinancing comes with it's own costs too: $3,154.03

- appraisal fee $300

- credit report $15

- commitment fee $245

- underwriting fee $160

- flood zone certification $10

- overnight fee $20

- interest 6/19/09-7/1/09 $186.56

- hazard insurance $218.04

- county property taxes $1665.93

- aggregate account adjustment -$163.50

- settlement or closing fee $110

- title insurance $220

- recording fee $40

- assignment fee $76

- overnight fee $20

Before you start saying that it looks like we made some poor financial decisions, let me remind you that when you are getting squeezed by your budget you will start to make choices that under other circumstances you would not. And you will justify it by saying it is the responsible thing to do. No one wants to pay more in interest than they have to! But in the long run whatever we saved was essentially wasted on fees, and additional interest. In the short term we survived another day.

When I total all the fees that were associated with this house in both obtaining a mortgage and then refinancing it (not counting property taxes) we spent $1,842.99 the first time and $1,488.10 the second time for a grand total of $3,331.09.

$3,331.09 for FEES and we are going to have thousands more in fees when it closes (that post will be fun). Regardless of what the housing market, or interest rates are doing there are fees everywhere! Fewer on the front end, and more on the back end. There is no way around it when you buy.

Owning a house is EXPENSIVE getting in, staying in, and getting out.

Next: The Mortgage Payment Breakdown

Wednesday, March 14, 2012

The Mistake My Budget Couldn't Recover From, Ever.

It is the single largest expense of nearly every budget: Housing.

In my original estimates I wrongly assumed that the only thing that would change in our expense equation was the cost of housing. We previously didn't have any, so I looked at our budget compared to our anticipated income and came up with what I thought we could reasonably afford.

Using my target number of $950/month I set out to find a house that would fit our price range and needs for our family. Thanks to the Internet you can research home prices all over the country. And thanks to the Internet you don't really get the full picture of what that house will cost.

I figured that at $950/month we could afford a house in the $135,000-$145,000 range (in 2006). I should add that $950/mo would be our top end. But then I started to discover that the seemingly affordable housing in the area we were relocating to wasn't as affordable as the numbers made it seem thanks to property taxes. Property taxes are a mere annoyance in some areas of the country, like where we were from. Property taxes in other parts of the country represent a large % of the costs associated with housing, like where we were going.

All of a sudden the price range we had to look in to meet the $950/month that I thought we could safely be in dropped dramatically to about $100,000. See in our state property taxes run on the low side about $2,500/year to $5,000/year about the low-average. Finding a home that was in good condition, that would meet our needs over the next 6 years was all but impossible to do in one week.

That probably explains why the realtor we were working with started showing us more expensive homes than the ones we asked to look at. Not to mention that she had a personal stake in showing us more expensive homes, her commission was based off the sales price!

When she showed us the house we eventually bought we were skeptical that we could afford it (those gut feelings are usually right), but the bank assured us that we could. What does the bank know about how I spend my money or what is important to me. What did they care about how many children we had, or if we ate rice and beans for every meal. Did they care that we would never take a vacation, see a movie, or get a babysitter? No.

On top of that we only had a week to look at potential properties. We had already spent so much time looking that turning back and starting over seemed to represent a failure on our part. What was the point of spending the money to come out to look if we went home empty handed.

Rentals? We had already convinced ourselves that we were going to buy a house. See, we were finally responsible adults with a family, and that is what people in our stage of life do. Don't fall for the lie. Buying is a good decision for some people, in some situations, in the right areas, under the right conditions. Interns and residents aren't always those people.

In the end we convinced ourselves that we could squeeze an extra $300 out of our budget. Really? Where did we think it would come from? We were so naive! To think we could eat less, drive less, buy less than we did as medical student with more children coming was just plain stupid. But the really foolish thing was to think that this house would never need any maintenance - that it would just take care of itself.

No Home Is Self-Sufficient! Over the last 6 years we spent $20,000 maintaining this home. That works out to an extra $277/month every month. Add that to the $300 we thought we could squeeze out of our budget and our budget was squeezing us by almost $600/month - just for a house, and that was before our property taxes increased.

Buying a house stretched our budget to the breaking point. We took on a mortgage larger than we felt we could handle, and we were right. But then as any homeowner will tell you, a house can be a money pit. You want to make your house your home. That means paint. With new paint all of a sudden your furniture looks drab and sad (we waited 3 years before we bought a piece of furniture). You don't go to movies so you watch HGTV all day.

You think of all these little DIY project that don't cost much, but pretty soon every dollar adds up. The free piece of furniture you are going to refinish may look great, but when the supplies are all purchased - free is now $40 and you didn't have time to go grocery shopping so it's fast food for dinner. Paint may be cheap, but you have to buy supplies that go along with painting.

A yard is nice, but now you have to buy a lawn mower. How about a snow shovel and other yard implements so your neighbors don't report you to the authorities for yard neglect. What about the tools you have to purchase to fix things yourself so you don't have to pay someone to do it for you... it all costs money.

Does your budget have the room? What are you willing to sacrifice just to say you own a home?

ADVICE: Don't buy a house before you start internship. WAIT. Move into a rental for 6 months. Get a feel for your new income. Get a feel for what your expenses will be in a new city/state. Get to know the area. Pay attention to the things that come up (car repairs, medical bills, etc). Monitor your expenses. If you feel your budget can handle buying a house and all the things that come with it, Great! And because you are renting you can take your time and find just the right place without being under undo pressure.

Next: How Much Does Buying A House Cost?

In my original estimates I wrongly assumed that the only thing that would change in our expense equation was the cost of housing. We previously didn't have any, so I looked at our budget compared to our anticipated income and came up with what I thought we could reasonably afford.

Using my target number of $950/month I set out to find a house that would fit our price range and needs for our family. Thanks to the Internet you can research home prices all over the country. And thanks to the Internet you don't really get the full picture of what that house will cost.

I figured that at $950/month we could afford a house in the $135,000-$145,000 range (in 2006). I should add that $950/mo would be our top end. But then I started to discover that the seemingly affordable housing in the area we were relocating to wasn't as affordable as the numbers made it seem thanks to property taxes. Property taxes are a mere annoyance in some areas of the country, like where we were from. Property taxes in other parts of the country represent a large % of the costs associated with housing, like where we were going.

All of a sudden the price range we had to look in to meet the $950/month that I thought we could safely be in dropped dramatically to about $100,000. See in our state property taxes run on the low side about $2,500/year to $5,000/year about the low-average. Finding a home that was in good condition, that would meet our needs over the next 6 years was all but impossible to do in one week.

That probably explains why the realtor we were working with started showing us more expensive homes than the ones we asked to look at. Not to mention that she had a personal stake in showing us more expensive homes, her commission was based off the sales price!

When she showed us the house we eventually bought we were skeptical that we could afford it (those gut feelings are usually right), but the bank assured us that we could. What does the bank know about how I spend my money or what is important to me. What did they care about how many children we had, or if we ate rice and beans for every meal. Did they care that we would never take a vacation, see a movie, or get a babysitter? No.

On top of that we only had a week to look at potential properties. We had already spent so much time looking that turning back and starting over seemed to represent a failure on our part. What was the point of spending the money to come out to look if we went home empty handed.

Rentals? We had already convinced ourselves that we were going to buy a house. See, we were finally responsible adults with a family, and that is what people in our stage of life do. Don't fall for the lie. Buying is a good decision for some people, in some situations, in the right areas, under the right conditions. Interns and residents aren't always those people.

In the end we convinced ourselves that we could squeeze an extra $300 out of our budget. Really? Where did we think it would come from? We were so naive! To think we could eat less, drive less, buy less than we did as medical student with more children coming was just plain stupid. But the really foolish thing was to think that this house would never need any maintenance - that it would just take care of itself.

No Home Is Self-Sufficient! Over the last 6 years we spent $20,000 maintaining this home. That works out to an extra $277/month every month. Add that to the $300 we thought we could squeeze out of our budget and our budget was squeezing us by almost $600/month - just for a house, and that was before our property taxes increased.

Buying a house stretched our budget to the breaking point. We took on a mortgage larger than we felt we could handle, and we were right. But then as any homeowner will tell you, a house can be a money pit. You want to make your house your home. That means paint. With new paint all of a sudden your furniture looks drab and sad (we waited 3 years before we bought a piece of furniture). You don't go to movies so you watch HGTV all day.

You think of all these little DIY project that don't cost much, but pretty soon every dollar adds up. The free piece of furniture you are going to refinish may look great, but when the supplies are all purchased - free is now $40 and you didn't have time to go grocery shopping so it's fast food for dinner. Paint may be cheap, but you have to buy supplies that go along with painting.

A yard is nice, but now you have to buy a lawn mower. How about a snow shovel and other yard implements so your neighbors don't report you to the authorities for yard neglect. What about the tools you have to purchase to fix things yourself so you don't have to pay someone to do it for you... it all costs money.

Does your budget have the room? What are you willing to sacrifice just to say you own a home?

ADVICE: Don't buy a house before you start internship. WAIT. Move into a rental for 6 months. Get a feel for your new income. Get a feel for what your expenses will be in a new city/state. Get to know the area. Pay attention to the things that come up (car repairs, medical bills, etc). Monitor your expenses. If you feel your budget can handle buying a house and all the things that come with it, Great! And because you are renting you can take your time and find just the right place without being under undo pressure.

Next: How Much Does Buying A House Cost?

Tuesday, March 13, 2012

My Budget Exposed

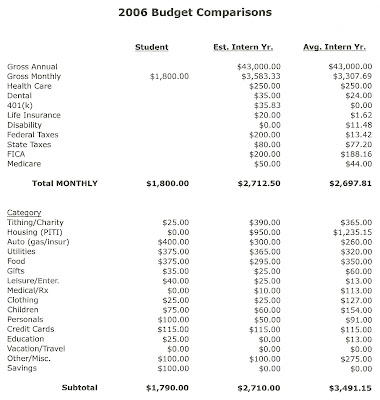

Here is a look at our first year. I was SOOOOO prepared. I spent hours, days, weeks working on this (6 years ago). You see as soon as we found out where we were matching I hit the numbers hard. I came up with a budget that I thought would work, based of course on how we had been living that year, payroll calculators, tax estimators and then tweaked a little to make it work (e.g., forced it to work). I was congratulating myself for my responsible approach and wise calculations.

As medical students we were poor, or I thought we were poor. We were living in my DrH parent's second home so we had no rent, we did pay utilities, but even then our income was gone. Granted it was a large metropolitan city in the west and just insuring our cars was expensive, not to mention cooling a house in the summer. But we didn't do anything! We did have a baby and one on the way ($$). But I am not kidding when I say we didn't do anything.

I was foolish to believe that we could continue living like we were then long-term, and even more foolish to believe that the only thing that would change in our budget equation was a mortgage payment. That I could somehow keep everything else constant. Life was going to teach me a lesson the hard way. No matter how much you plan and prepare, if you don't plan for the "what if" you aren't prepared.

I am going to admit right now that I am embarrassed when I look at this budget. Another benefit of anonymity. Even with all my knowledge about budgeting, even though I had been successful at it, I still fell into traps. The same traps that are waiting for you. Even with all my best laid plans my budget didn't have any room to breathe. In my calculations, nothing could go wrong 6 years. That just isn't likely. By Christmas we had used up all our savings and were financially suffocating.

I am feeling the need to defend my spending to you. When I look at it I am appalled that I was so "off" when I made my estimated budget and what actually happened. The only pleasant surprise in the whole thing was that is cost less to insure our cars in our new state so we saved a little money there. But just a little. Everything else was more than I expected. We just bought a house! I was pregnant! We were having a new baby! We had the baby! Our toddler grew!

This wouldn't just be a one time deal either. How were we supposed to survive the next 5 1/2 years? How did this happen to me, I thought I was prepared? This wasn't supposed to happen.

I also want to point out that I had a line item on our budget for credit card payments. I previously said that from the day we married we committed to never put anything on a credit card that we couldn't pay off that next month and we have lived that way ever since. Unfortunately, before we were married we weren't so disciplined and had one credit card with a balance of $4,000 that we made monthly payments on until the day it was paid off nearly two years ago. That was $115 dollars a month out of our budget for those years that we were spending on something(s) we purchased and consumed in the past when we probably didn't need it. Using credit is robbing your future at precisely the same time your future needs it! I am unaware of a credit card that will allow you to charge without making payments. They have to be paid, and your budget cannot afford it.

What you will see next is really three budgets. The first is the one we were living with during medical school. The second I projected while planning for internship/residency. And the third was reality in internship/residency (an average of the months July-Dec).

As medical students we were poor, or I thought we were poor. We were living in my DrH parent's second home so we had no rent, we did pay utilities, but even then our income was gone. Granted it was a large metropolitan city in the west and just insuring our cars was expensive, not to mention cooling a house in the summer. But we didn't do anything! We did have a baby and one on the way ($$). But I am not kidding when I say we didn't do anything.

I was foolish to believe that we could continue living like we were then long-term, and even more foolish to believe that the only thing that would change in our budget equation was a mortgage payment. That I could somehow keep everything else constant. Life was going to teach me a lesson the hard way. No matter how much you plan and prepare, if you don't plan for the "what if" you aren't prepared.

I am going to admit right now that I am embarrassed when I look at this budget. Another benefit of anonymity. Even with all my knowledge about budgeting, even though I had been successful at it, I still fell into traps. The same traps that are waiting for you. Even with all my best laid plans my budget didn't have any room to breathe. In my calculations, nothing could go wrong 6 years. That just isn't likely. By Christmas we had used up all our savings and were financially suffocating.

I am feeling the need to defend my spending to you. When I look at it I am appalled that I was so "off" when I made my estimated budget and what actually happened. The only pleasant surprise in the whole thing was that is cost less to insure our cars in our new state so we saved a little money there. But just a little. Everything else was more than I expected. We just bought a house! I was pregnant! We were having a new baby! We had the baby! Our toddler grew!

This wouldn't just be a one time deal either. How were we supposed to survive the next 5 1/2 years? How did this happen to me, I thought I was prepared? This wasn't supposed to happen.

I also want to point out that I had a line item on our budget for credit card payments. I previously said that from the day we married we committed to never put anything on a credit card that we couldn't pay off that next month and we have lived that way ever since. Unfortunately, before we were married we weren't so disciplined and had one credit card with a balance of $4,000 that we made monthly payments on until the day it was paid off nearly two years ago. That was $115 dollars a month out of our budget for those years that we were spending on something(s) we purchased and consumed in the past when we probably didn't need it. Using credit is robbing your future at precisely the same time your future needs it! I am unaware of a credit card that will allow you to charge without making payments. They have to be paid, and your budget cannot afford it.

So, go ahead and say that this won't happen to you. You will be better prepared, you will make better decisions, you will be different. But what if you aren't? What will you do?

Next: The Mistake My Budget Couldn't Recover From

Next: The Mistake My Budget Couldn't Recover From

Monday, March 12, 2012

A Close Look At Expenses

A budget deals with two items: income and for expenses. We have previously covered what you might expect on the income side as a new intern/resident. Now let's talk about expenses.

Most people live on a fixed income. They may make more or less than average but their income still stays about the same every single month. Would you be surprised to know that people who make several hundred-thousand dollars a year run into the same kind of money problems as people who bring in much less? The issue is not how much money you make, it's the way you spend your money that makes the difference.

Do you know what your expenses (obligatory and non-obligatory) are and the frequency in which the occur?

Do you know what expenses you might incur in the future?

When I started budgeting I learned something very quickly. I couldn't use a budget created by someone else. The ones that say you should spend x% on rent, x% on food, x% on movies, etc. I am not generic, I am unique and so are my expenses. No two people are going to spend their money in exactly the same way, that's why only you can make your budget. I could do it for you, but guess what... you wouldn't like it and it would not respect your priorities for your money - it would reflect mine!

You have to do it yourself (or with your spouse/significant other). The good news is it is not difficult.

If you don't already know what your expenses are it might be tempting to guess. That would be a fun exercise! You see expenses are a lot like calories. I always think I eat less than I actually do. Same goes for spending. If I didn't already know what I spend on certain categories I would be very surprised by some of the results. So if you are interested in seeing how close or far from reality you are, try making an estimate.